health insurance marketplace texas

According to the results from my search, there are several ways to get health insurance in Texas, depending on your eligibility and preferences. Here are some of the options:

- You can use HealthCare.gov, the federally run health insurance exchange, to purchase ACA Marketplace plans from private insurers. If you buy coverage from an exchange, you may be eligible for tax credits to help pay your premiums1.

- You can contact your state Department of Insurance for consumer assistance with a health insurance problem or question

- You can apply for Medicaid in Texas by contacting your state Medicaid office Medicaid is a program that provides health coverage for low-income individuals and families.

- You can check your children’s eligibility for CHIP (Children’s Health Insurance Program), which covers too many uninsured children in middle-income families to qualify for Medicaid

- You can also explore alternatives such as Marketplace Insurance Exchange or HealthMarkets Insurance which are independent insurance companies that offer a variety of health insurance plans, including individual, group, Medicare, dental, vision, and supplemental plans around

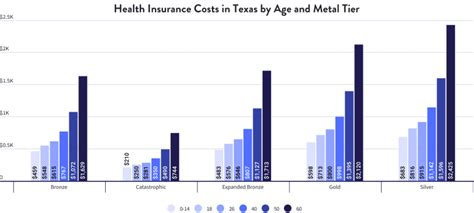

What is the cost of health insurance in Texas

The cost of health insurance in Texas depends on several factors, such as your age, location, plan type, and income. According to the results from my search, the average cost of health insurance in Texas across all tiers is $469 per month a decrease of 6% between 2022 and 2023. However, the actual cost may vary greatly depending on your specific situation and eligibility for financial assistance.

Some of the cheapest health insurance plans in Texas for each metal tier are as follow

- Catastrophic: CHRISTUS Catastrophic – 3 free PCP visits, including virtual ($314 per month)

- Copper: Moda Select Texas Standard Copper ($321 per month)

- Extended Bronze: Community Choice Bronze 016 (limited network, no cancellation for PCP & Generics, free 24/7 telehealth) ($323 per month);

- Silver: Community Choice Silver 019 (limited network, no deductible for PCPs, specialists and generics, free 24/7 telehealth) ($445 per month);

- Gold: Community Choice Gold 022 (limited network, no deductible for PCPs, specialists and generics, free telehealth 24/7) ($393 per month).

You can use the Texas Healthcare Costs

What is the difference between metal tiers

The difference between metal tiers is how you and your insurance company split the costs of your health care. The four metal tiers are Bronze, Silver, Gold, and Platinum. They have nothing to do with the quality of care or the benefits covered by the plans

Here is a summary of how the cost sharing works for each metal tier

| Plan Category | The insurance company pays | You pay |

|---|---|---|

| Bronze | 60% | 40% |

| Silver | 70% | 30% |

| Gold | 80% | 20% |

| Platinum | 90% | 10% |

Generally, plans with higher premiums have lower deductibles and copayments, meaning you pay less when you use health care services. Plans with lower premiums have higher deductibles and copayments, meaning you pay more when you use health care services.

You should choose a metal tier that suits your budget and health care needs. For example, if you expect to use a lot of care, you may want to choose a Gold or Platinum plan that covers more of your costs. If you want to save on monthly premiums and don’t expect to use much care, you may want to choose a Bronze or Silver plan that covers less of your costs.

What is a deductible

A deductible is the amount of money that you have to pay for covered health care services before your insurance plan starts to pay. For example, if your plan has a $1,000 deductible, you will have to pay the first $1,000 of your medical bills in a year, and then your insurance will cover the rest of the costs. The deductible is separate from the premium, which is the amount you pay every month to keep your insurance active. The deductible is also different from the copay or coinsurance, which are the amounts you pay for each service or medication after you meet your deductible.

The size of the deductible can vary depending on the type of health insurance plan you have. Generally, plans with higher deductibles have lower premiums, and vice versa. You should choose a deductible that fits your budget and health care needs. If you expect to use a lot of health care services, you may want to choose a lower deductible so that your insurance covers more of your costs. If you want to save money on premiums and don’t expect to use much health care services, you may want to choose a higher deductible.